Australia (from where I’m from) has a wonderfully vulgar expression referring to stock prices: “They go up and down like a whore’s drawers.”

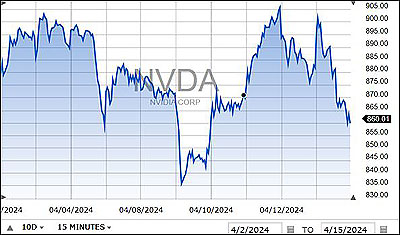

The American equivalent is Nvidia. In the last two weeks, it has gone up and down, and up and down:

My friend, the investment guru, says NVDA is going to $500 and I ought to sell. There are a bunch of investment analysts (who do guessing for a living) who think it could reach $1,200. It’s now just below $900.

I’ve been in tech since 1969. I’ve lived through many tech revolutions – from the invention of the microprocessor, to data communications, to fiber optic, to the Internet, to the communications satellite, to the mobile phone, to the cloud, to streaming video and now AI. Like all these other inventions, AI will touch and improve all companies and all of us. Nvidia is my largest stock holding — by far — and I’m not selling, though my paper profits are more than pleasing — or, as they say (again) in Australia, Nvidia has proven “better than a slap in the belly with a cold fish.”

While I wasn’t posting this blog, I spent the last two weeks reading, researching and listening, and concluded:

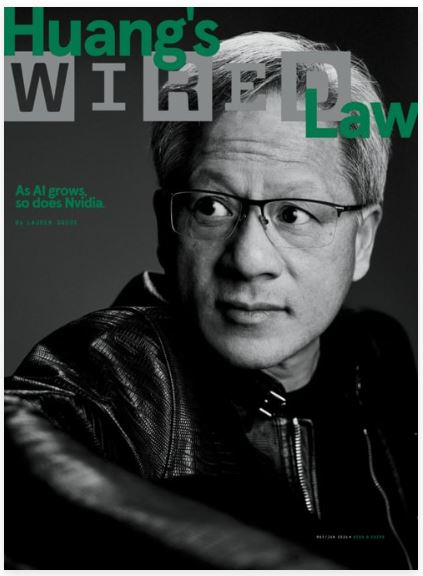

+ Jensen is brilliant at getting publicity for Nvidia. Look what just appeared in Wired.

Wiredwrote:

Nvidia Hardware Is Eating the World

Tech companies can’t get enough of this tech company. Earnings are off the charts. WIRED probes the mind of its CEO, Jensen Huang.

For the full article, click here.

+ AI is what Jeff Bezos called the cloud “market size unconstrained.”

+ Acquired’s podcasts are engrossing. I’ve just listened to Hermes. I’m now listening to Amazon Web Services. I’m buying more Amazon.

+ You can’t do enough reading, researching and listening.

+ Most every stock today is overpriced on conventional value measures.

+ We’re trading on feelings. emotion and enthusiasm. The two biggest areas as AI and fat drugs (NVO and LLY). The three BIG emotional areas are oil, bitcoin and gold. I now own a little oil (IEO), some bitcoin (via Fidelity), but not gold. I think I may have missed that bus.

+ Ultra-low interest rates (in fact stupidly-low interest rates) over the last 20 years seriously messed up the real estate biz. Then came work at home. Now three-times higher insurance rates (as a result of climate change) are sounding the death knell for many properties. I have examples. That’s for another day.

+ We’re never going to get to 2% inflation. The economy is far too strong. The Middle East mess will spike oil prices. Higher oil prices really mess with inflation.

+ When an autocrat gets power there’s no limit to the idiocy and pettiness of the decisions they make. For example, the Ayatollahs came to power in 1979 — that’s 45-years of unelected Supreme Leaders. One of their first decisions was to outlaw ballet in Iran. There was no “logic.” They just did it. Now there’s a movement outside Iran to revive it. This picture broke my heart. It’s a young Iranian ballet dancer who wants to dance in Iran.

You can read the full story here.

China’s dictator-for-life, Xi Jinping, allows anyone in China with a grievance (small or large) against a foreigner to obtain an Exit Ban. That means the American, European or Australian, etc. can’t leave the country for years — maybe never. Read more about this nonsense. click here.

+ If you’re a dictator, you have to find a cause to motive your subjects. For Iran, it’s eradicate the Jews. For other dictators, it’s other groups, like Muslims in China or Burma (now called Myanmar). I don’t get hatred against religion.

+ In my search for super AI applications, I found Topaz, photo enhancing software. Run it on your photos and watch it do its magic. Every other image editing software requires you, the user, to push buttons and mess around. Not Topaz. It’s AI on steroids. Try it on your family photos. You’ll be blown away. I’ll write more on it soon. For now, you should check it out yourself. Click here.

How AI develops — this is funny

In a New York Times review of a new novel,

Lydia Kiesling writes:

She’s an A.I. Sex Robot, and She’s Becoming Sentient

Sierra Greer’s debut novel, “Annie Bot,” explores questions of misogyny and toxic masculinity by following a pleasure robot that begins to develop her own consciousness.

In an unremarkable New York apartment, sometime in the not-too-distant future, a man tells his robot to come to bed. She is a “Stella,” an intelligent machine who looks and sounds like a woman. We soon learn that she is a “Cuddle Bunny,” a euphemistic term for the sex-robot setting she’s currently running. She is also set to “autodidactic” mode, which gives her a searching intellect and a nascent independence. Her name is Annie, and we will follow her on the journey to elevated consciousness in “Annie Bot,” Sierra Greer’s slyly profound debut novel.

Annie’s human is Doug, and she is programmed to read his moods and cater to his every need. “Annoyance, a 2 out of 10. She must be careful,” the close-third narration tells us. Her actions are calibrated to his pleasure. She knows, for instance, that during sex, “he does not like her too loud.”

Before she was set to Cuddle Bunny, Annie was set to “Abigail,” the robot’s house-cleaner mode. (Stellas also offer a “Nanny” mode for child-minding.) But as a Cuddle Bunny, Annie now forgets the crumbs on the counter and the dust under the couch, which angers the entitled and demanding Doug. He wishes he could toggle her back and forth from sex kitten to maid, but it would wreak havoc on her circuitry.

Through her autodidactic growth, Annie accumulates knowledge about everything from programming to literature, but she also learns more complex human truths as well – that there can be something exciting about having a secret, for example. But even as her consciousness advances, her existence remains circumscribed by Doug and her personality remains stunted by her need to please him. “Her core does not recognize authority in her voice,” she realizes when she tries to change her own settings. Our disgust with Doug grows as we watch him try to shape Annie into a misogynist’s dream of perfection.

I worry this overview makes the novel sound like an artless women’s lib 101 survey or a broad sendup of toxic masculinity. But Greer’s novel is, in fact, a brilliant pas de deux, grappling with ideas of freedom and identity while depicting a perverse relationship in painful detail.

The novel’s central conflict is between Annie’s development and her status as Doug’s possession. Ironically, Doug finds Annie’s increasing sentience alluring; the more human she becomes, the more he can pretend that she is truly his girlfriend. But Doug is in thrall to an entity whose equality he cannot accept, not only because she is a robot he bought for $220,000, but because ownership inflames the constitutional misogyny of an insecure, wounded man. Throughout the novel, he yo-yos between rigid control and minor concessions to her selfhood. Without exactly feeling sorry for Doug (I yearned for Annie to enter Terminator mode and rip him apart), I was struck by Greer’s nuanced portrait of a person whose soul is curdled by his exercise of power over another being.

There are moments when the novel strains credulity: We never learn how Doug earns enough money to purchase a custom sex robot, and despite living in an advanced technological era, he still has 783 analog books on his shelf. We do, however, learn that he is liberal. I suspect these details are meant to illustrate that erudition and liberal politics do not inoculate against misogyny, but they feel pat. The novel also gestures toward the significance of race and transgender identity in a world where humans and A.I. intermingle, but these ideas remain unexplored.

The novel’s sparse world-building and relatively quiet prose do not detract from its strength, though. Like Annie conserving the memory in her CPU, the novel marshals its real power to depict its central relationships.

The result is a gripping depiction of the ideologies that shape this novel’s world – and our own world too.

Donald Trump loves me

He has sent me 502 emails this year. I’m averaging five a day.

I originally subscribed to see what he was sending out. His stuff is remarkably creative. I like the one headed “Harry, do you still love me?“

Unsubscribing doesn’t work — surprise, surprise.

How to unsubscribe

Some emails have two options Unsubscribe or Update Profile

My latest “trick” is to change my profile to Harry@HarryJomes.com.”

At my desk, wired works best

I subscribe to one gigabit fiber. When I plug directly in my laptop says I’m getting 803.53 million bits per second. When I go on Wi-Fi, I get 112.18.

Plugging in is 7.2 times faster.

Favorite commentaries

The daffodils, forsythia, and white flowering trees are in full bloom. It’s nearly 60.

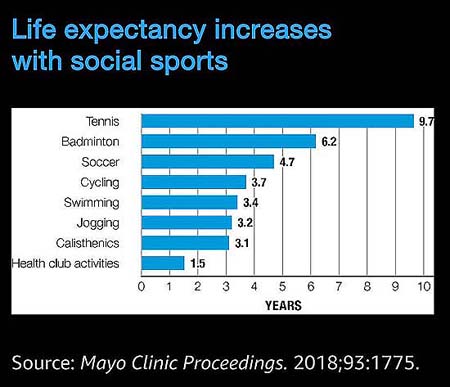

I’m going to play outside tennis outside at noon. Look what I found:

I’ll be back tomorrow. — Harry Newton